# load packages

library(tidyverse) # for data wrangling and visualization

library(tidymodels) # for modeling

library(usdata) # for the county_2019 dataset

library(openintro) # for Duke Forest dataset

library(scales) # for pretty axis labels

library(glue) # for constructing character strings

library(knitr) # for neatly formatted tables

library(kableExtra) # also for neatly formatted tablesf

# set default theme and larger font size for ggplot2

ggplot2::theme_set(ggplot2::theme_bw(base_size = 16))SLR: Simulation-based inference

Bootstrap confidence intervals for the slope

Sep 12, 2022

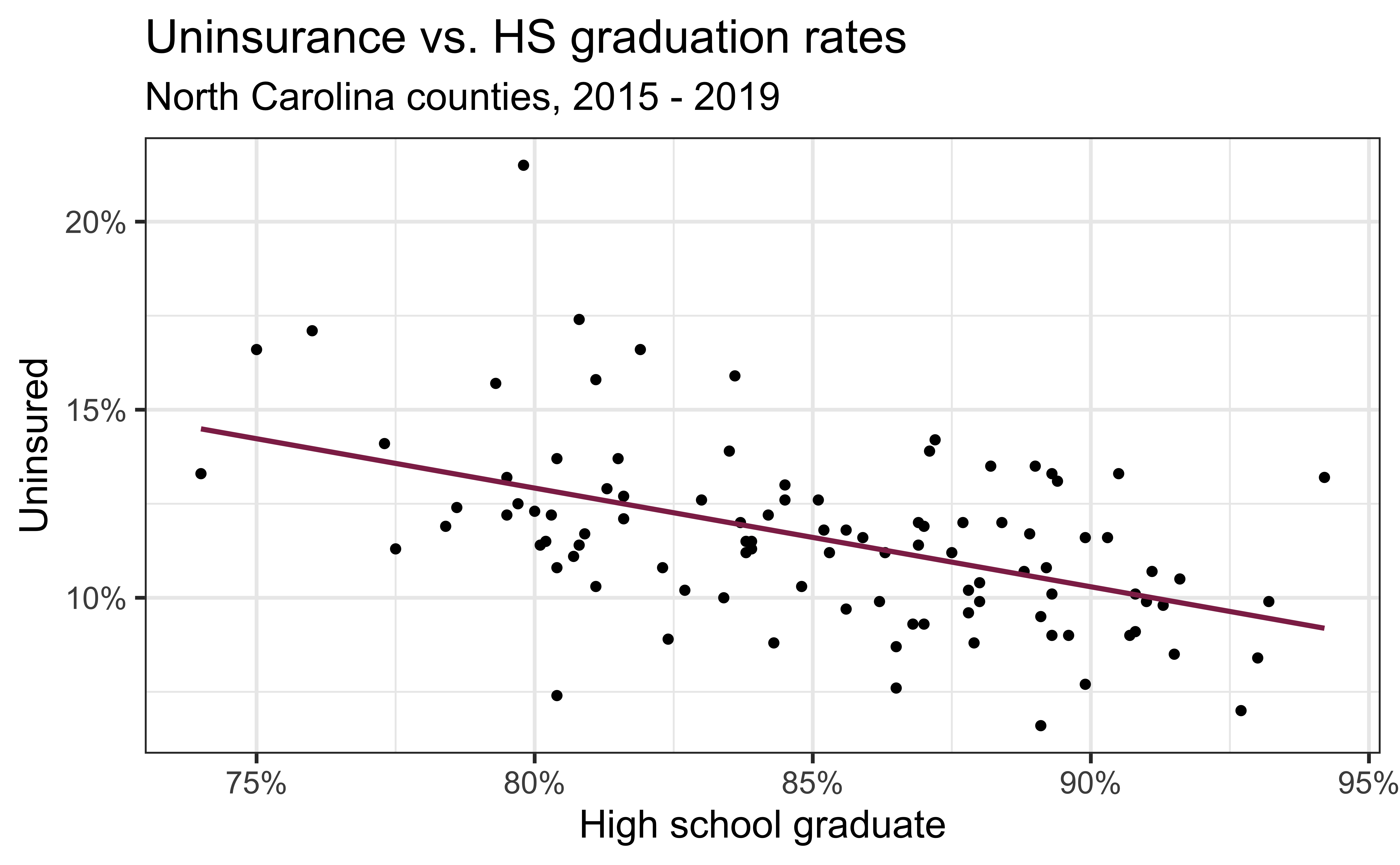

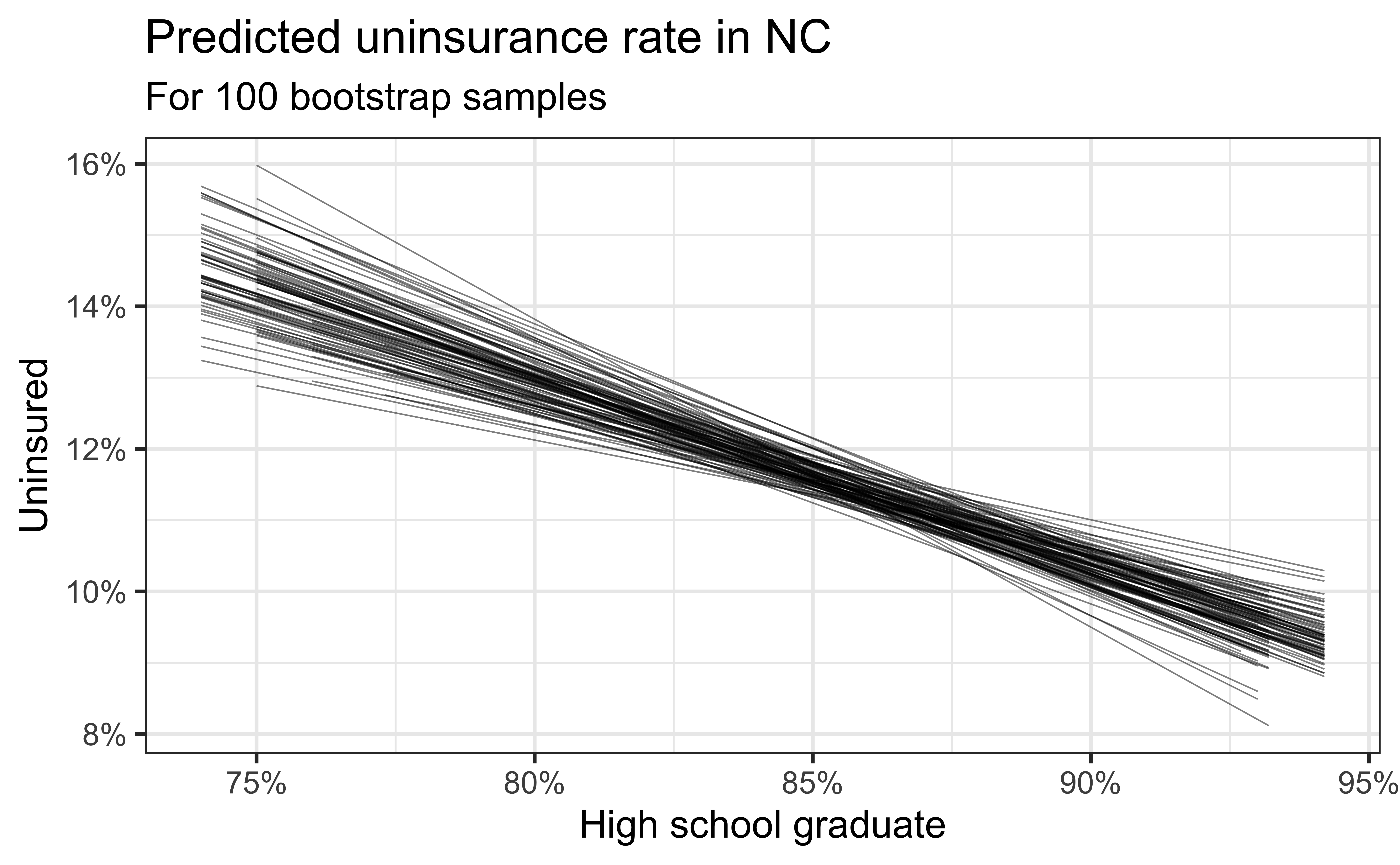

Uninsurance vs. HS graduation rates

Code

ggplot(county_2019_nc, aes(x = hs_grad, y = uninsured)) +

geom_point() +

geom_smooth(method = "lm", se = FALSE, color = "#8F2D56") +

scale_x_continuous(labels = label_percent(scale = 1, accuracy = 1)) +

scale_y_continuous(labels = label_percent(scale = 1, accuracy = 1)) +

labs(

x = "High school graduate", y = "Uninsured",

title = "Uninsurance vs. HS graduation rates",

subtitle = "North Carolina counties, 2015 - 2019"

)

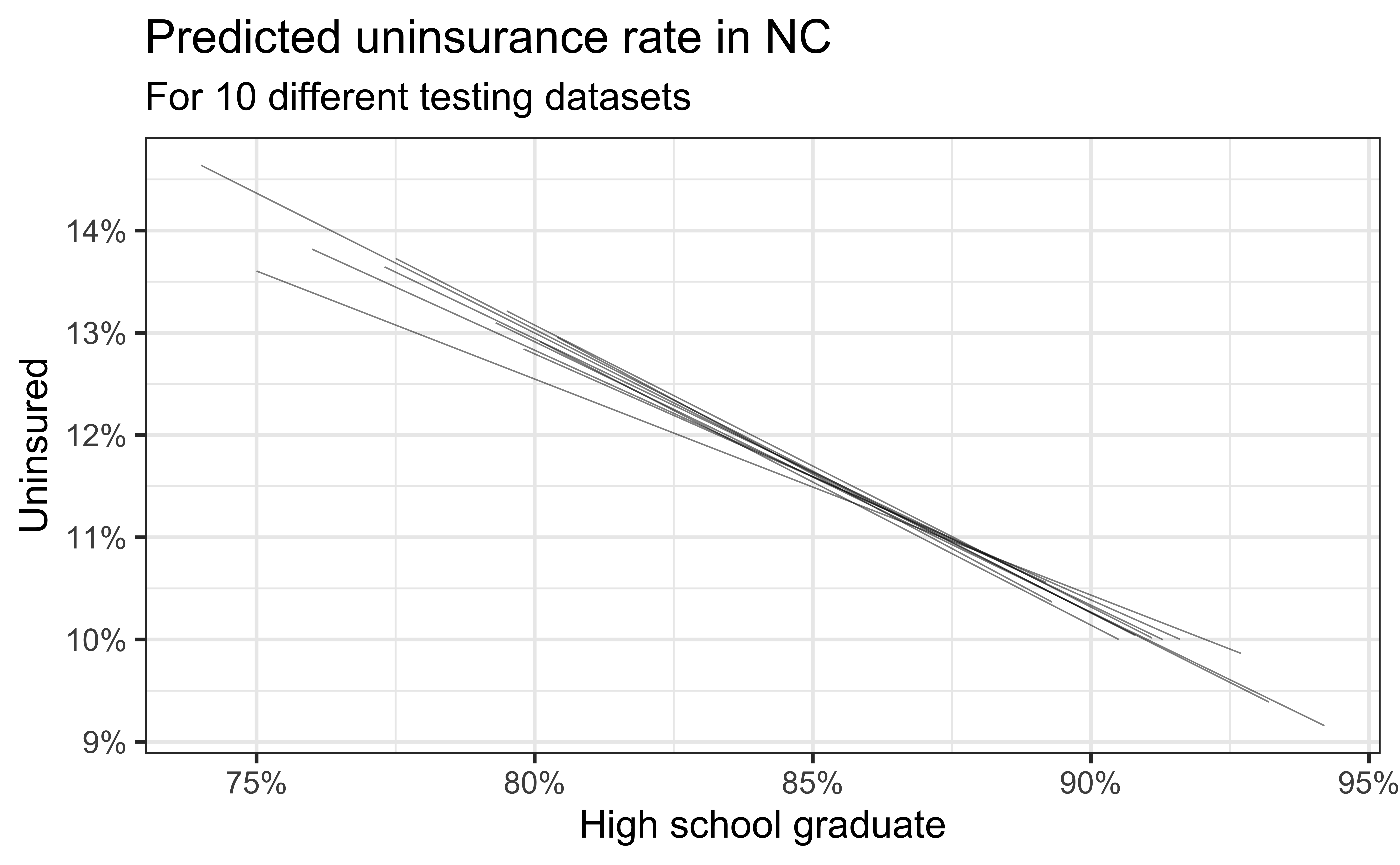

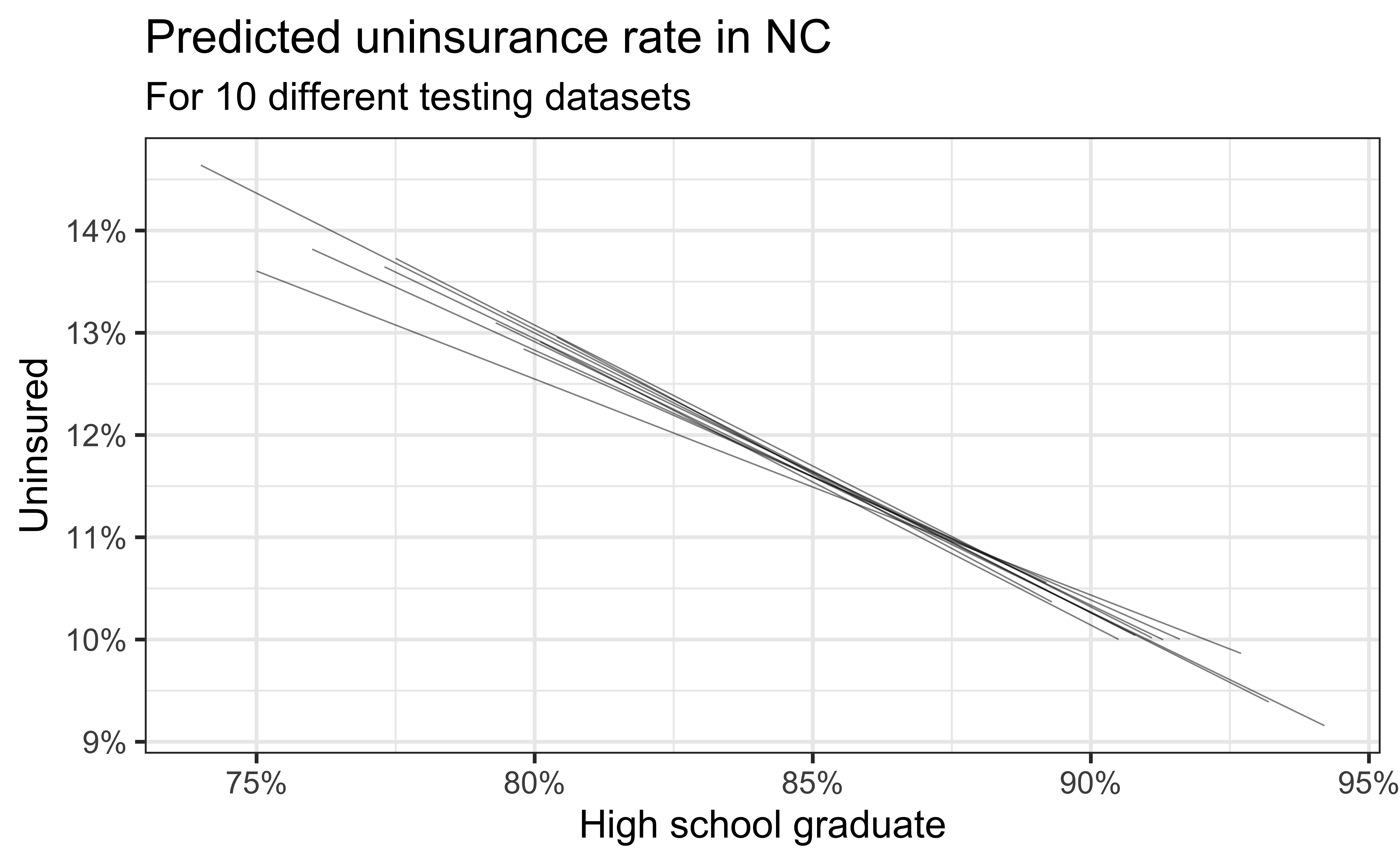

Simulation: data splitting

- Take a random sample of 10% of the data and set aside (testing data)

- Fit a model on the remaining 90% of the data (training data)

- Use the coefficients from this model to make predictions for the testing data

- Repeat 10 times

Predictive performance

- How consistent are the predictions for different testing datasets?

- How consistent are the predictions for counties with high school graduation rates in the middle of the plot vs. in the edges?

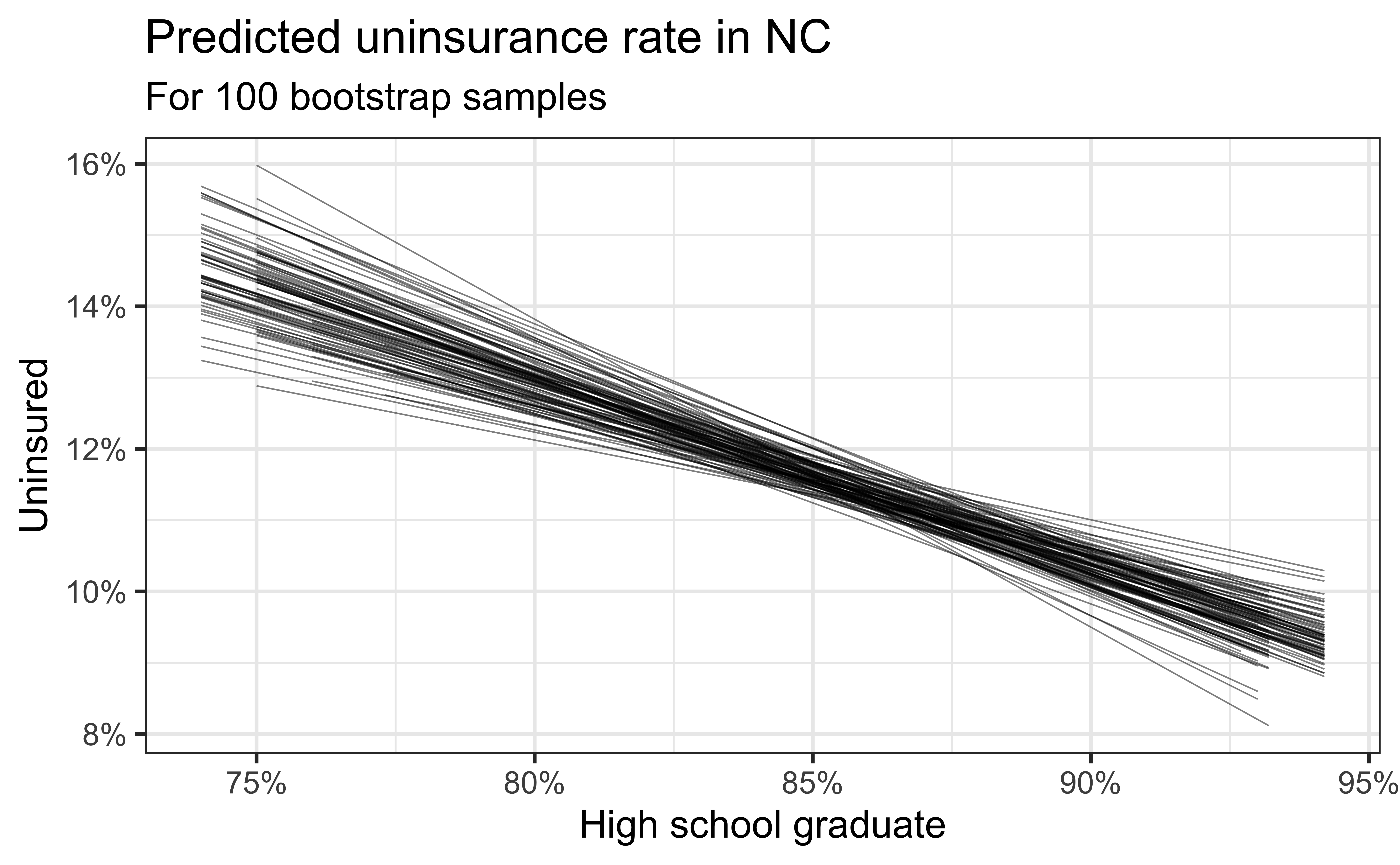

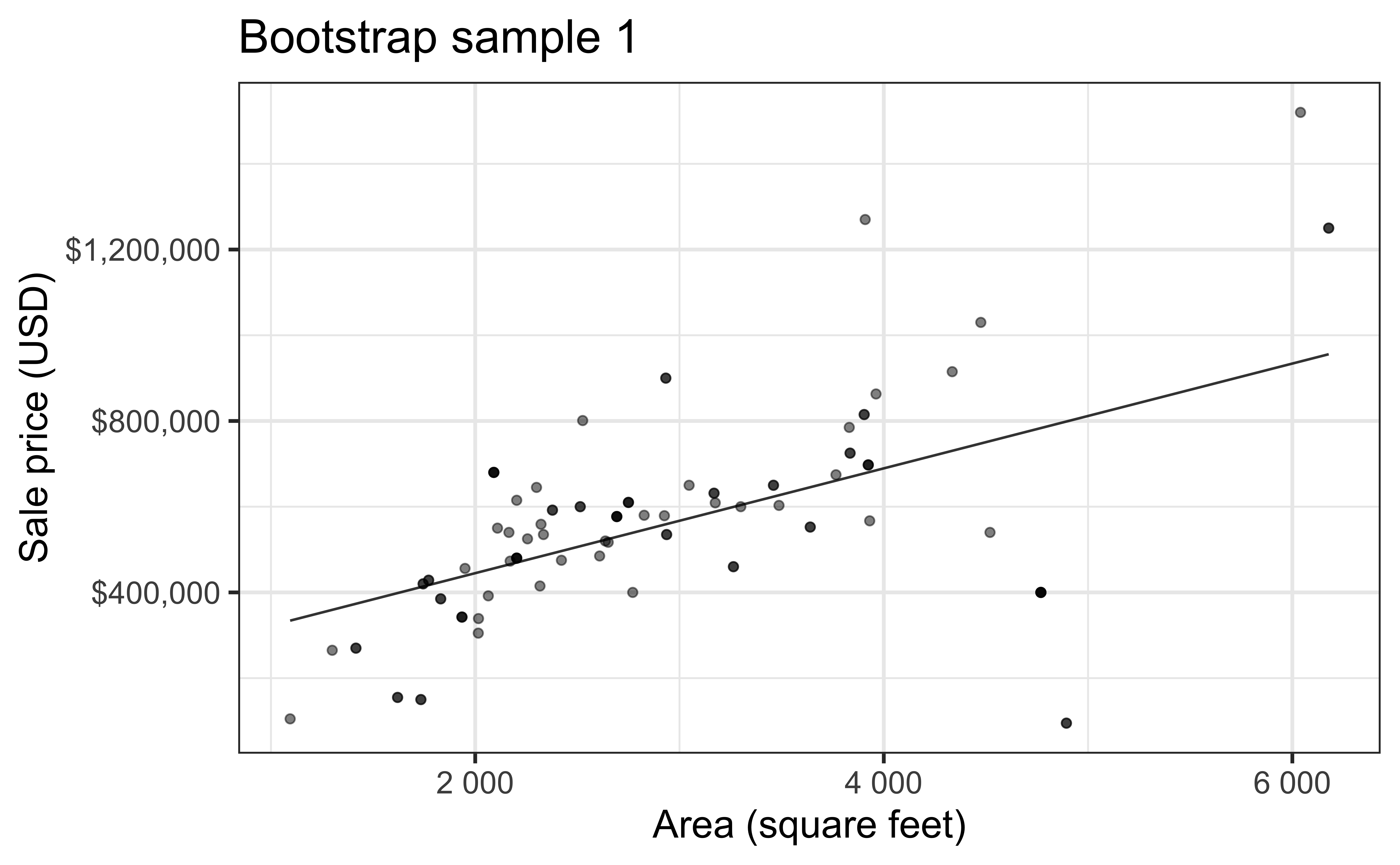

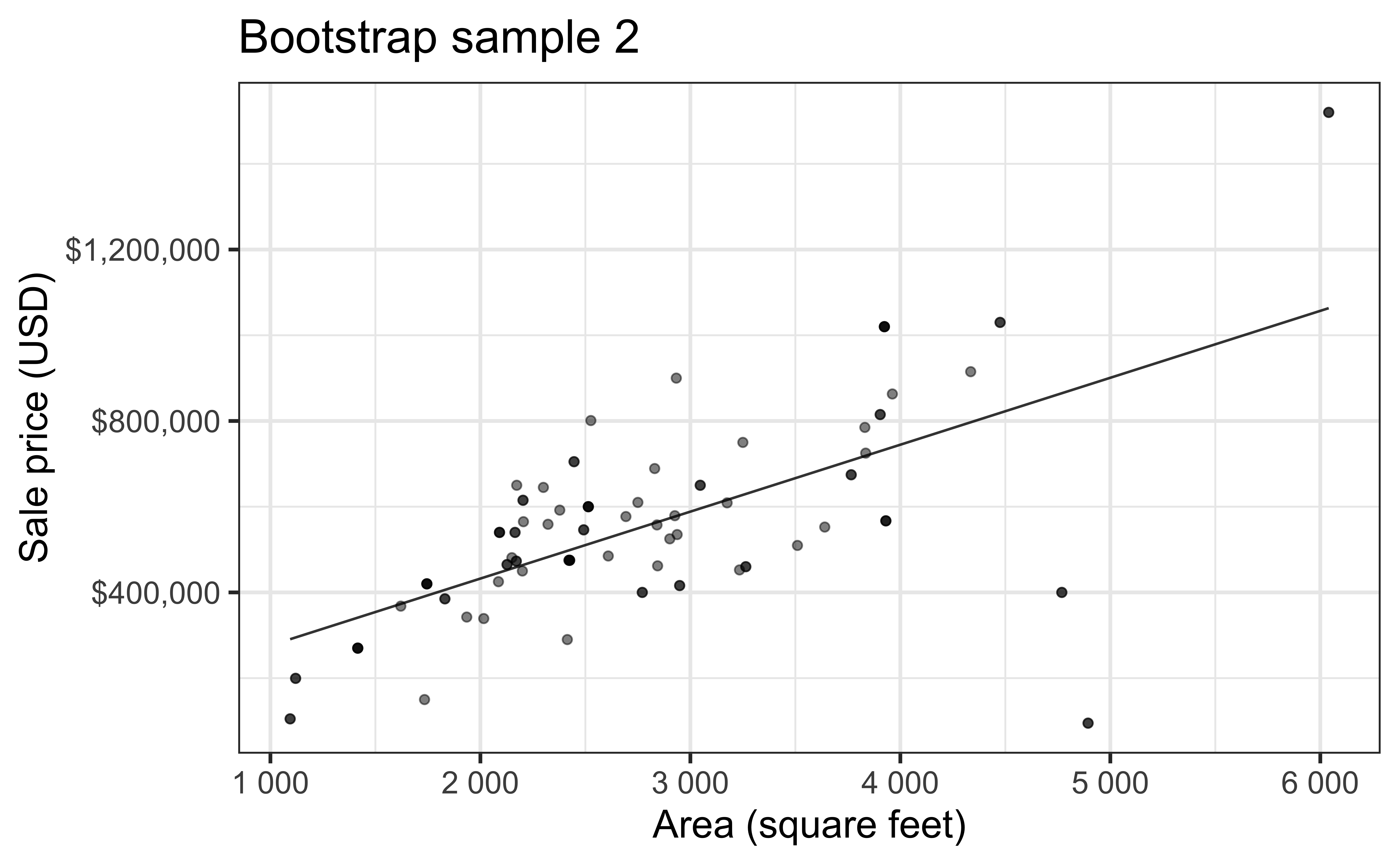

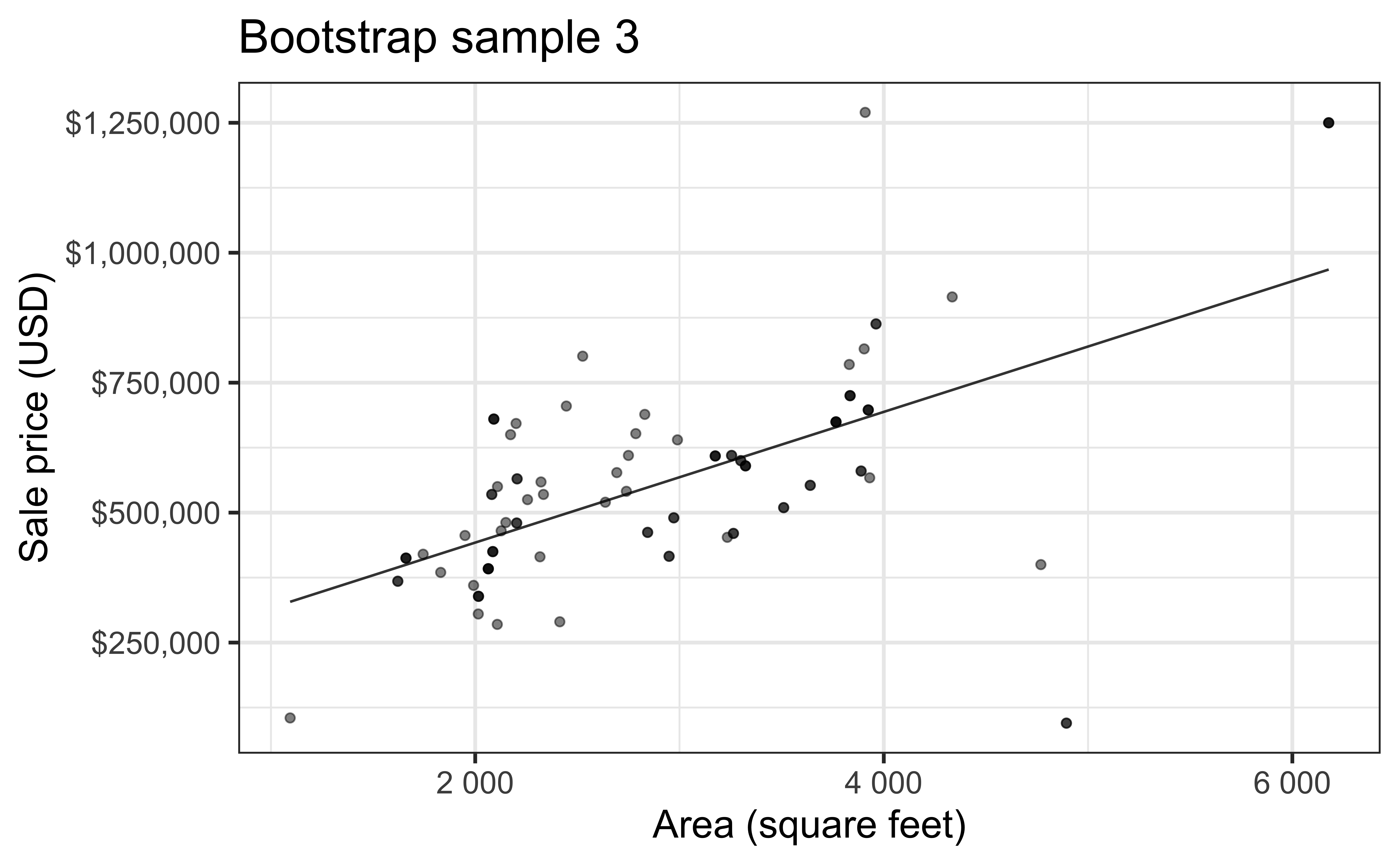

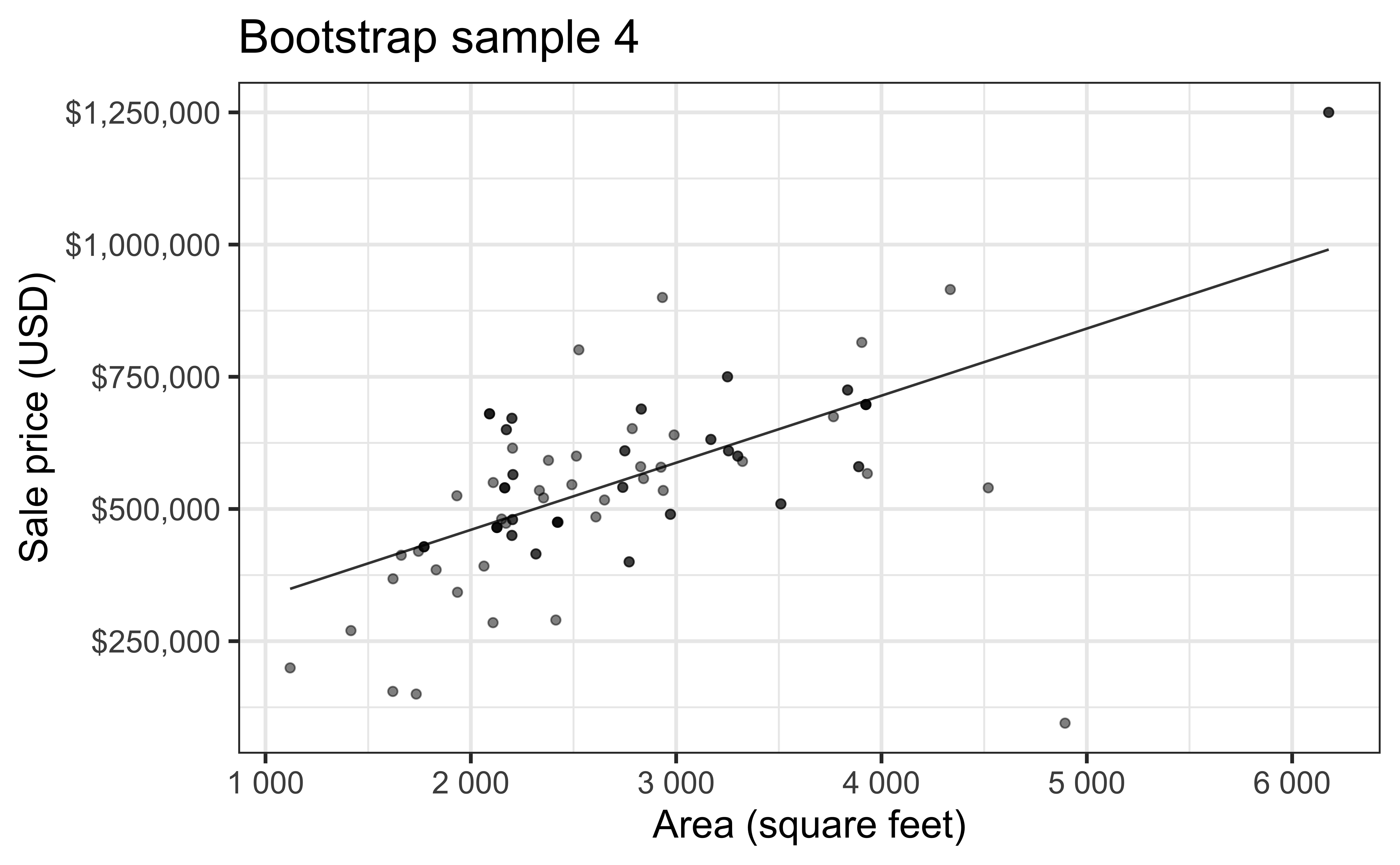

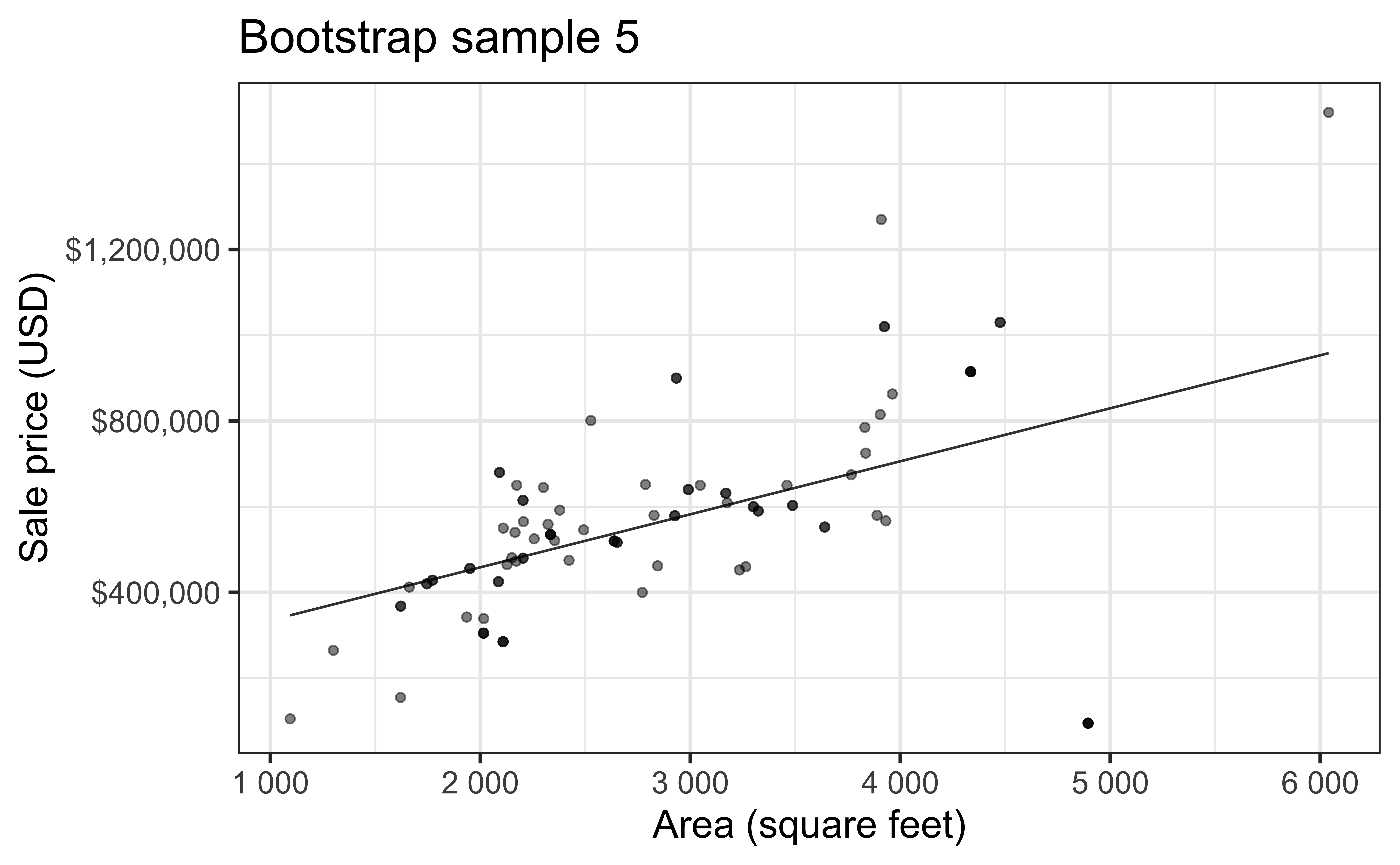

Simulation: bootstrapping

- Take a bootstrap sample – sample with replacement from the original data, same size as the original data

- Fit model to the sample and make predictions for that sample

- Repeat many times

Predictive performance

- How consistent are the predictions for different bootstrap datasets?

- How consistent are the predictions for counties with high school graduation rates in the middle of the plot vs. in the edges?

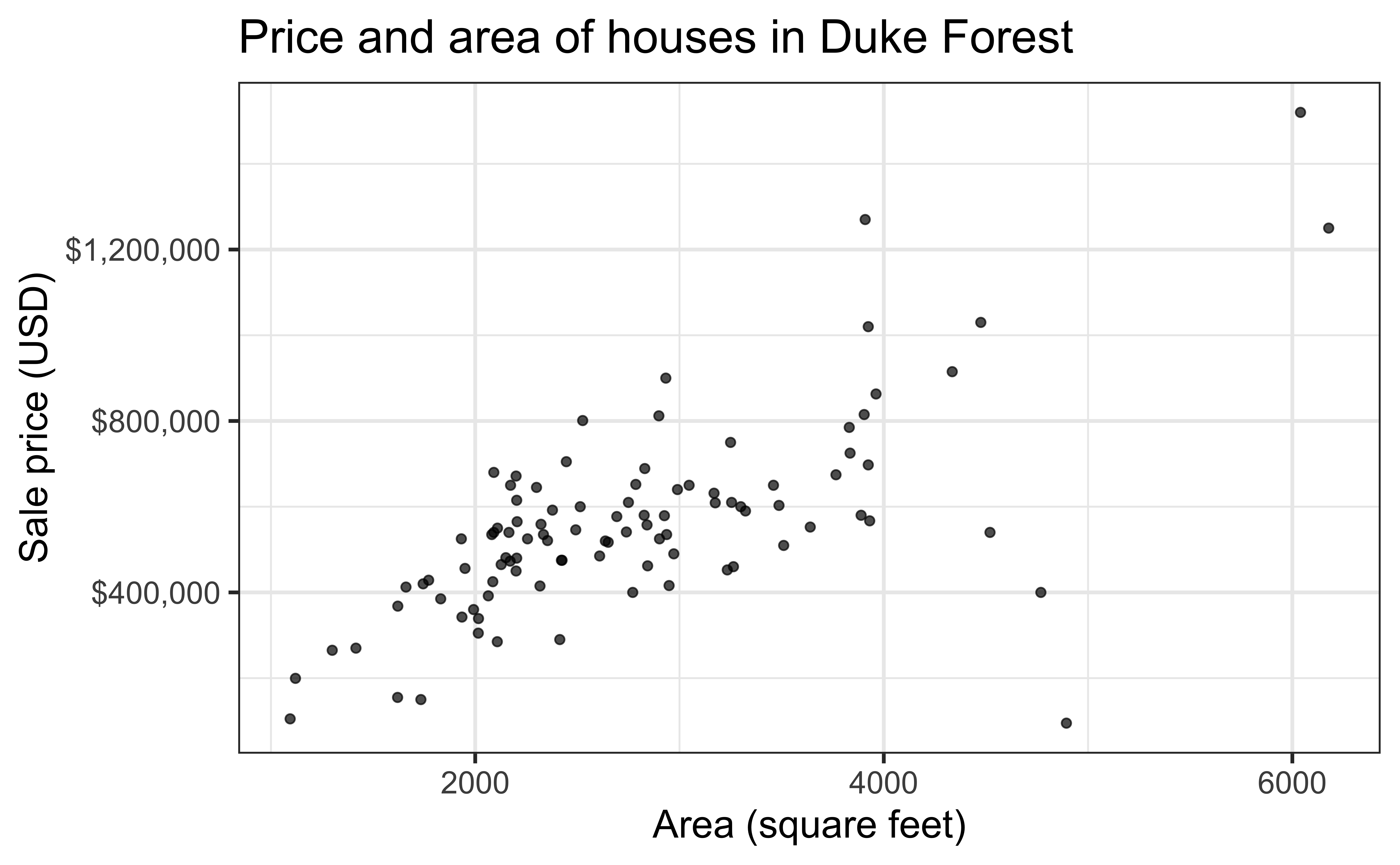

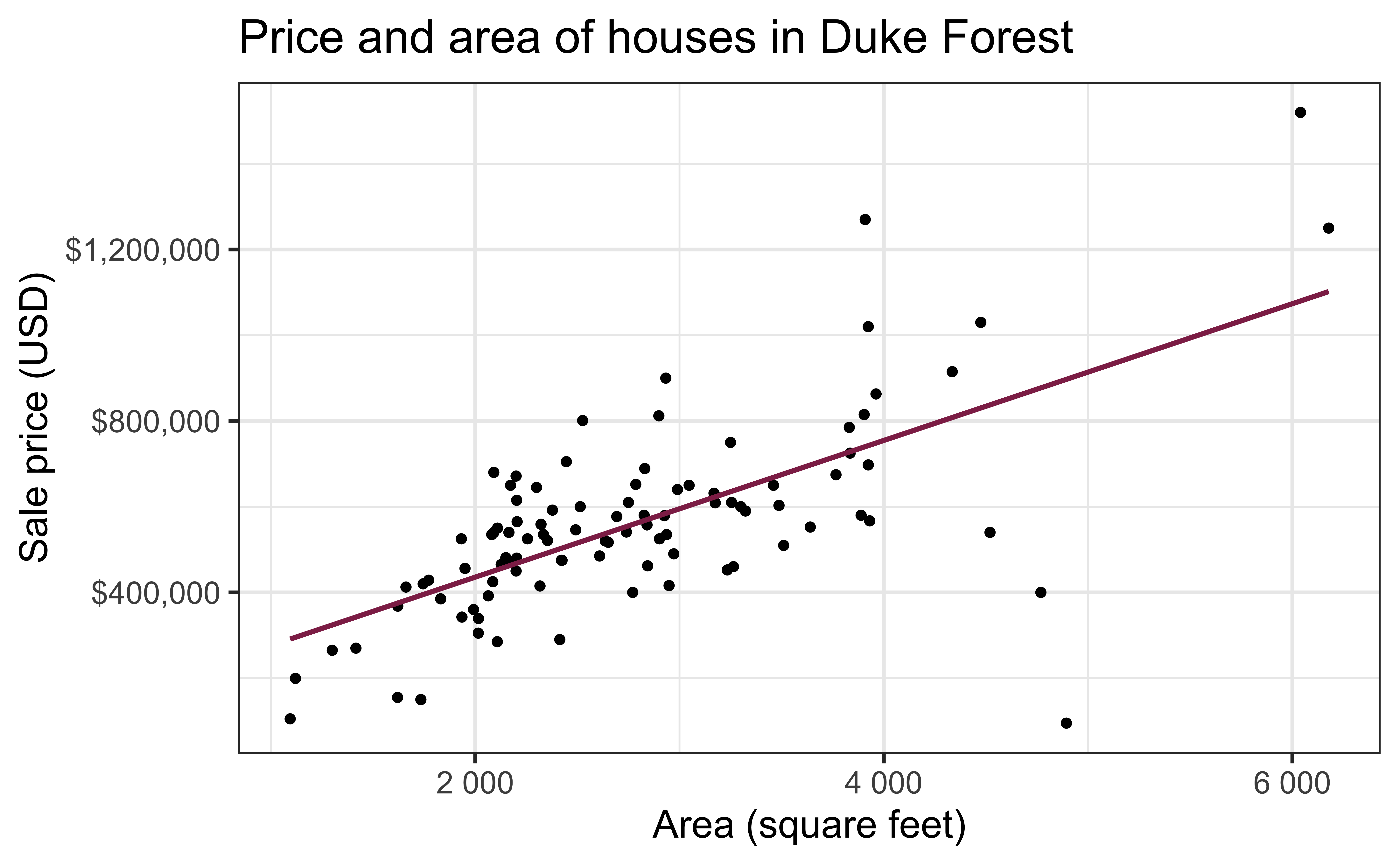

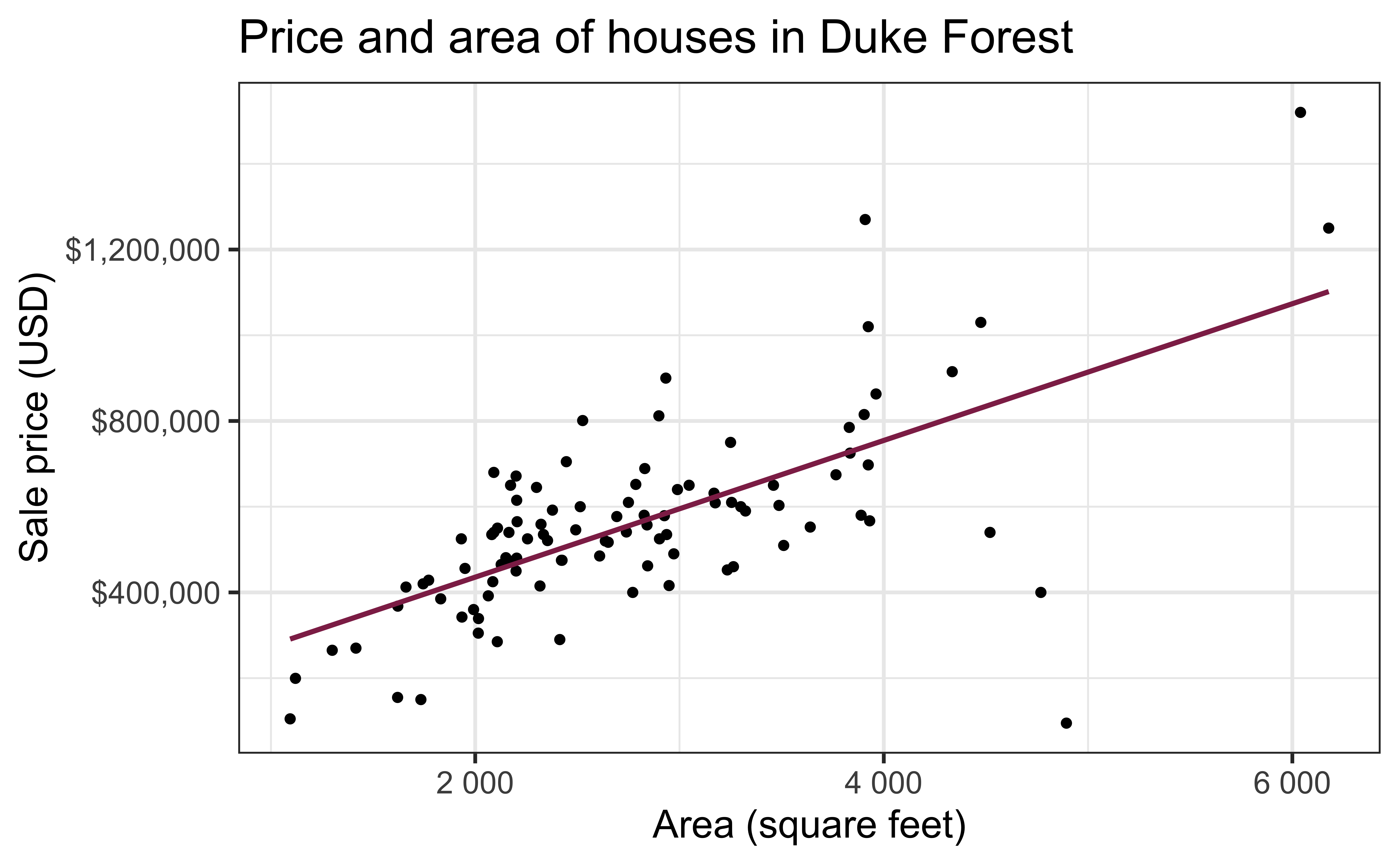

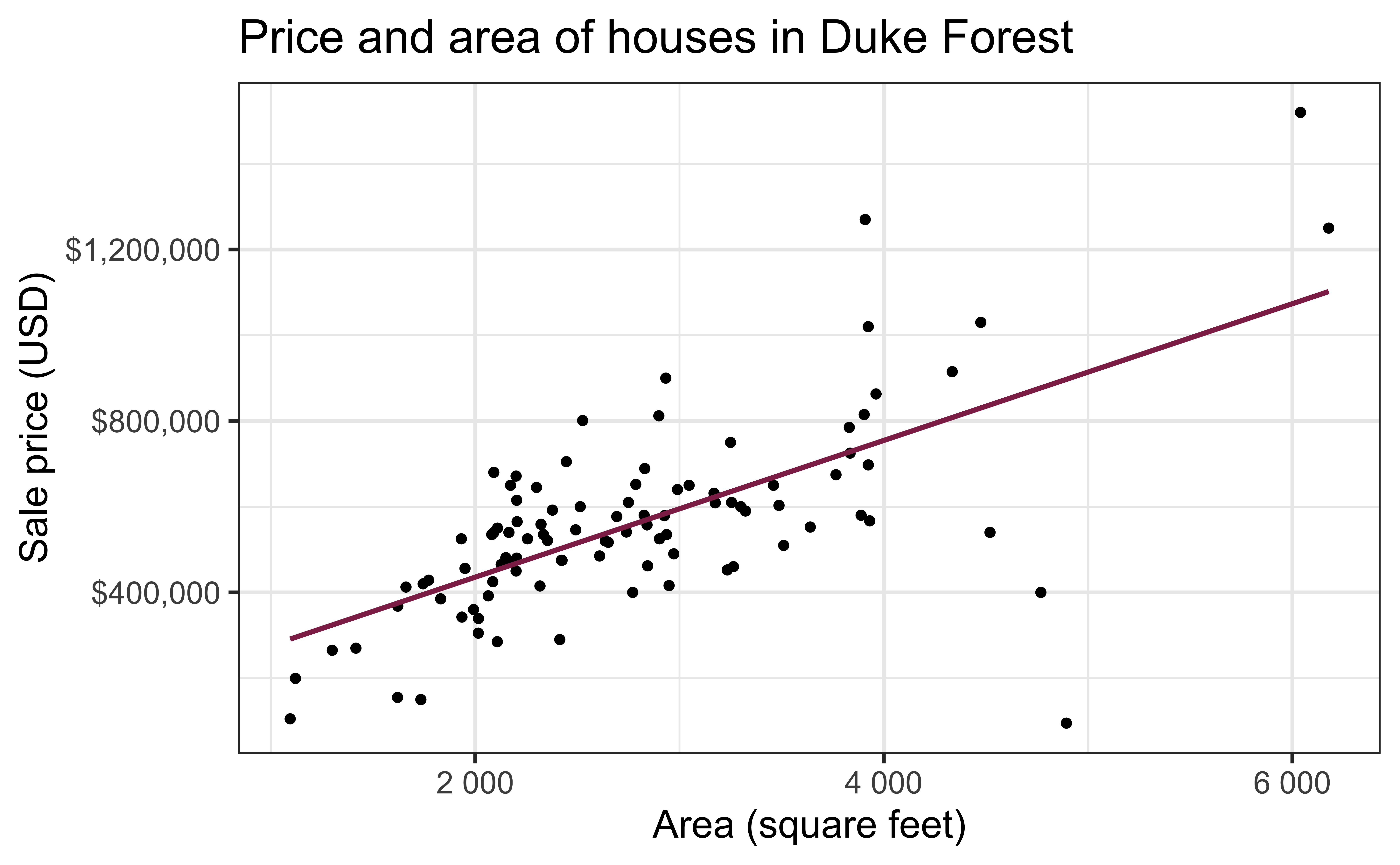

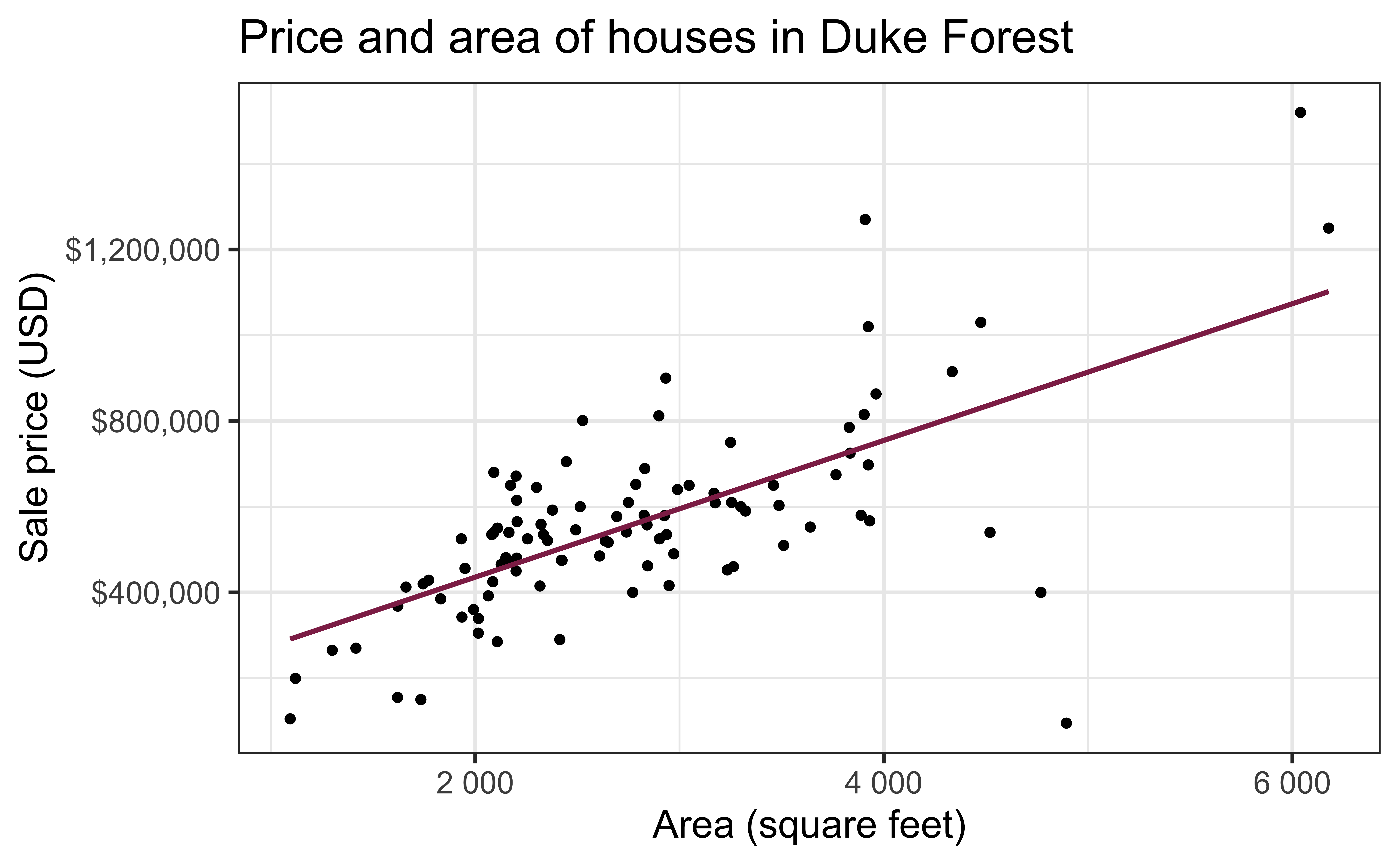

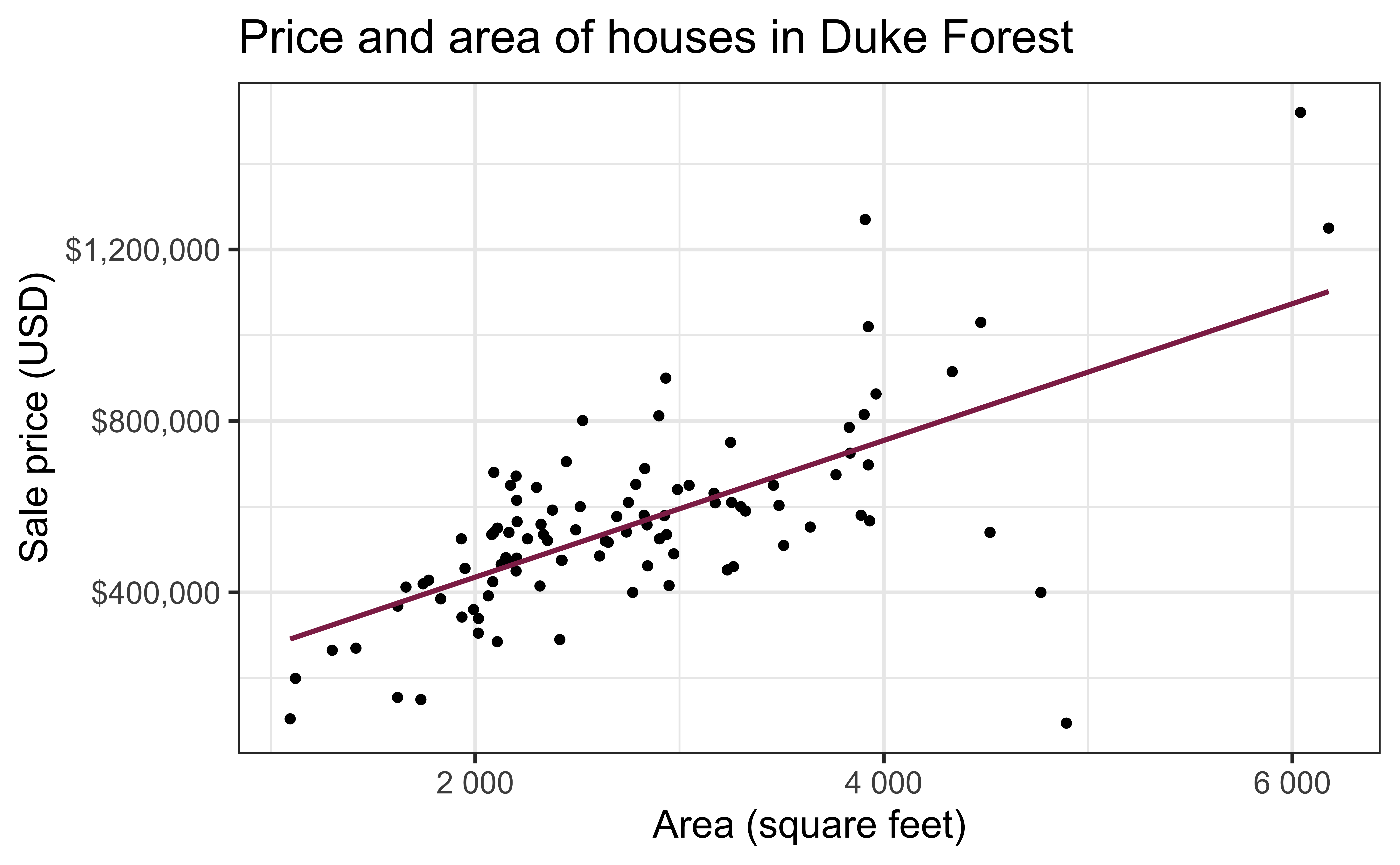

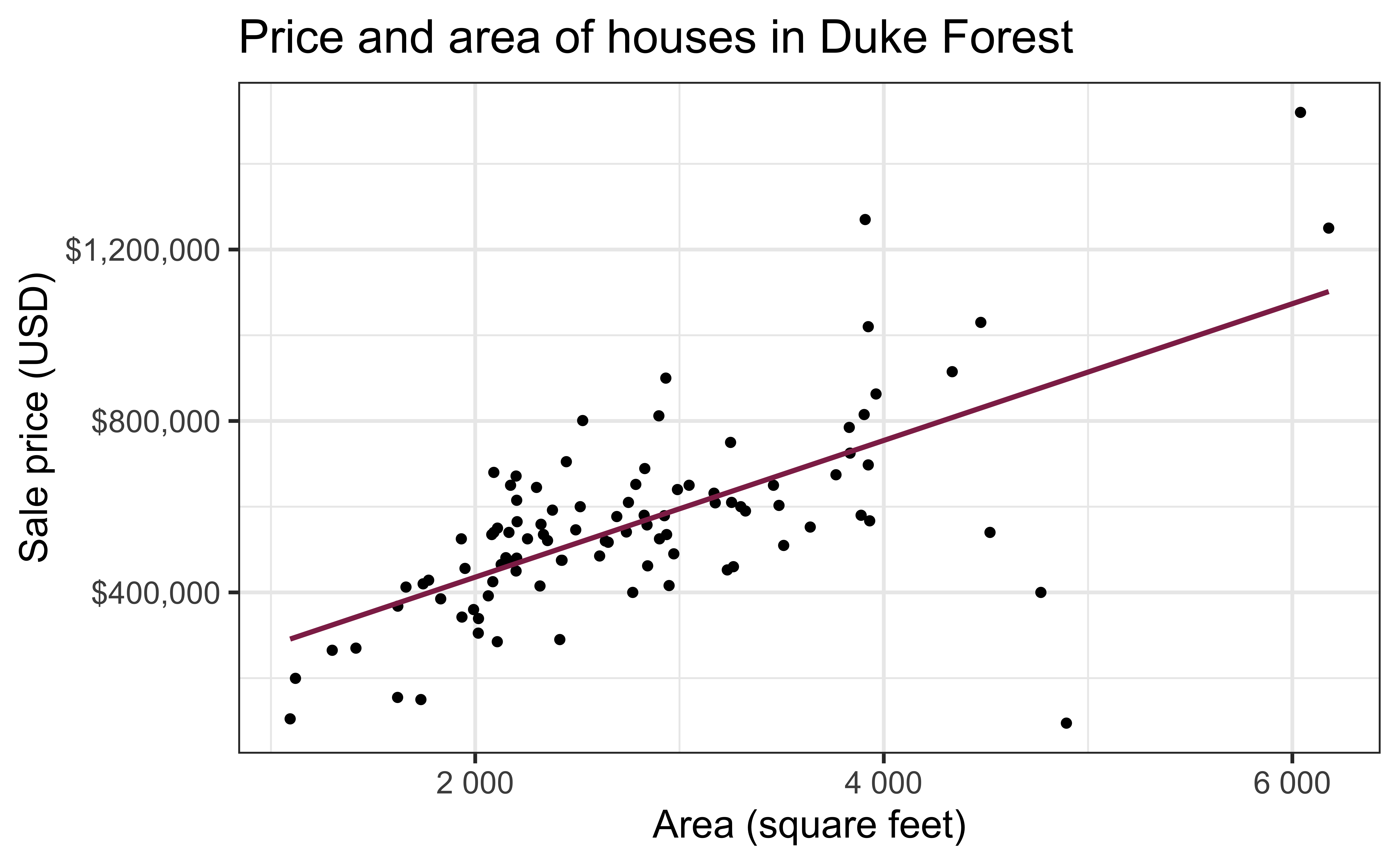

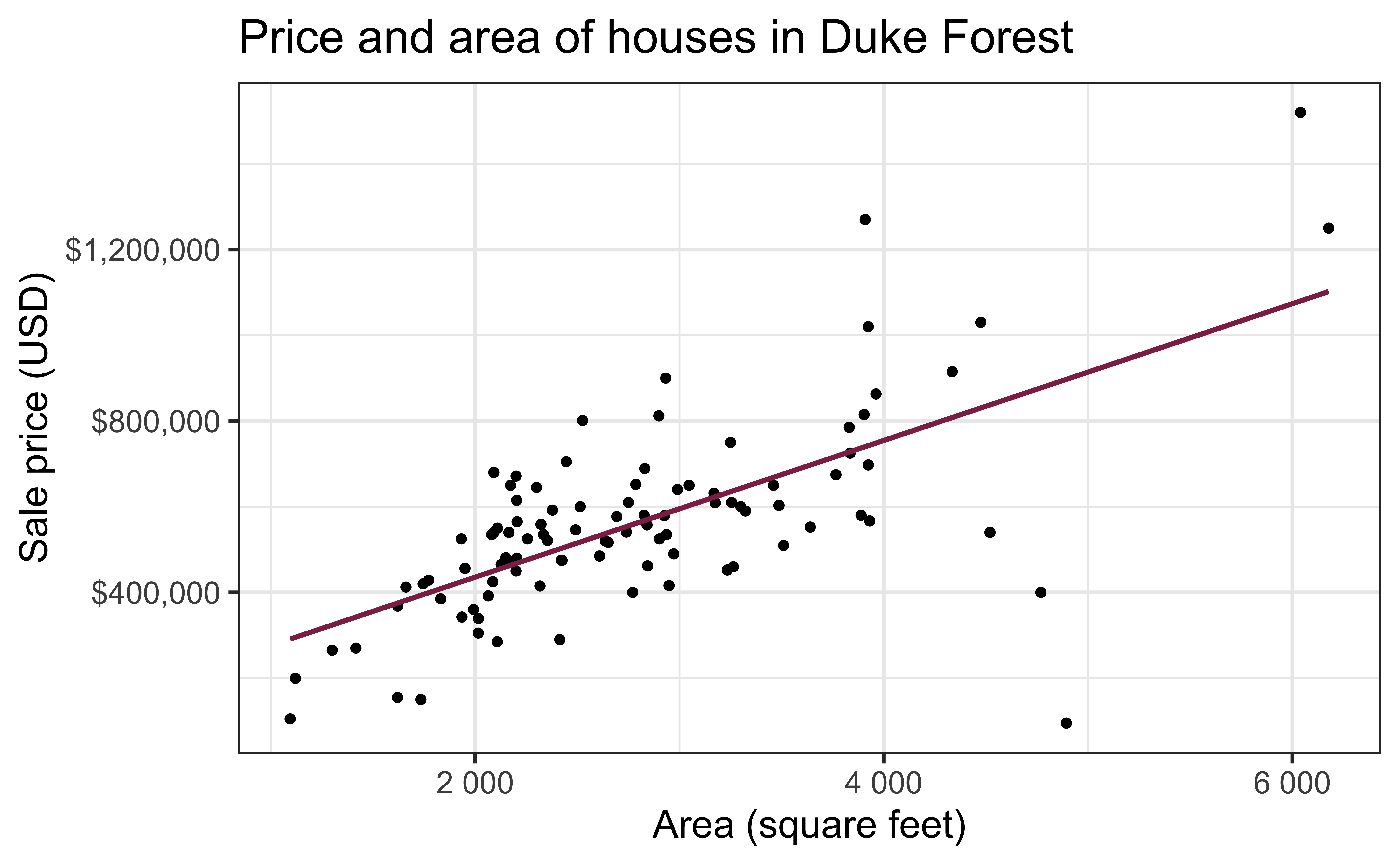

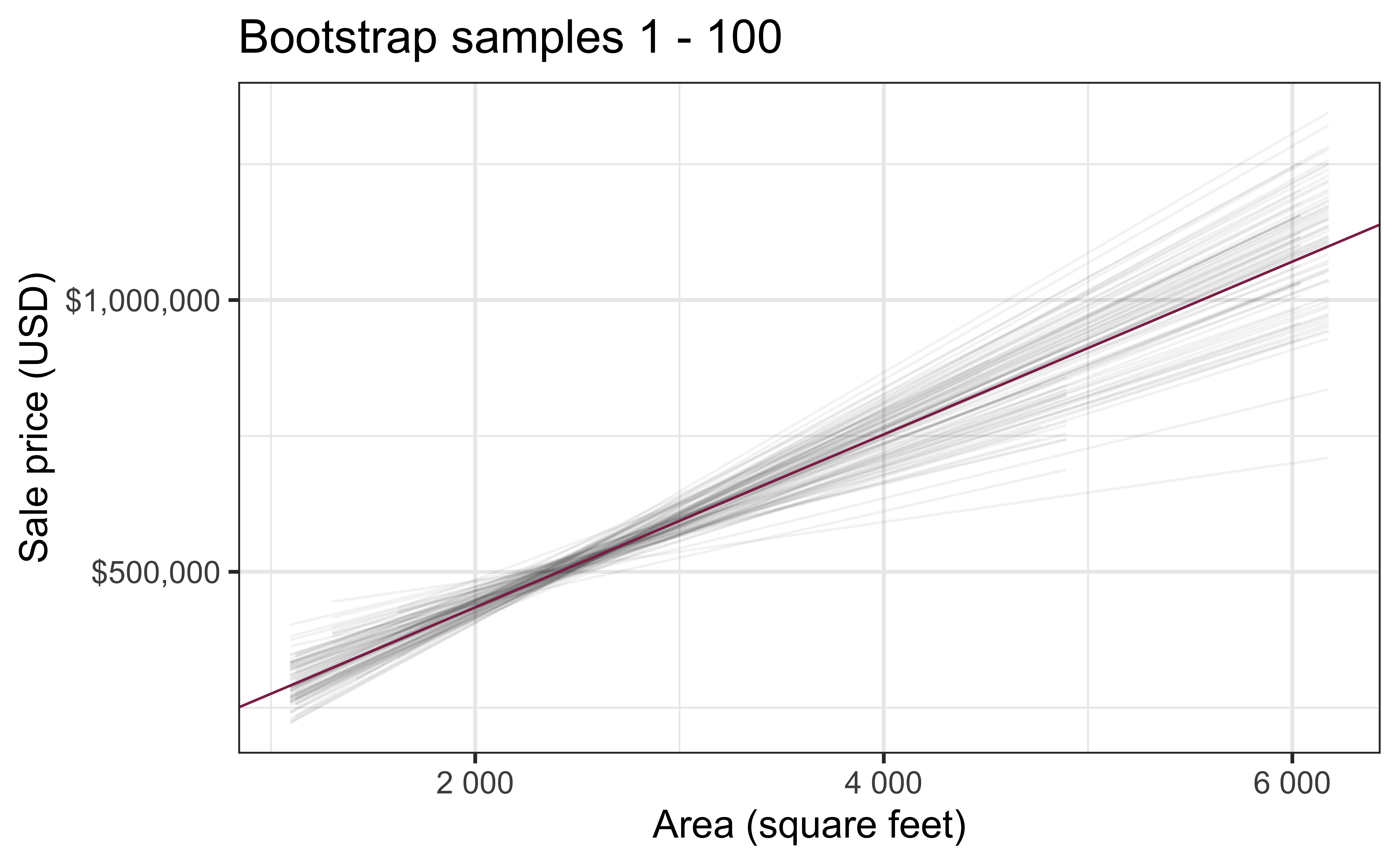

Data: Houses in Duke Forest

- Data on houses that were sold in the Duke Forest neighborhood of Durham, NC around November 2020

- Scraped from Zillow

- Source:

openintro::duke_forest

Goal: Use the area (in square feet) to understand variability in the price of houses in Duke Forest.

Exploratory data analysis

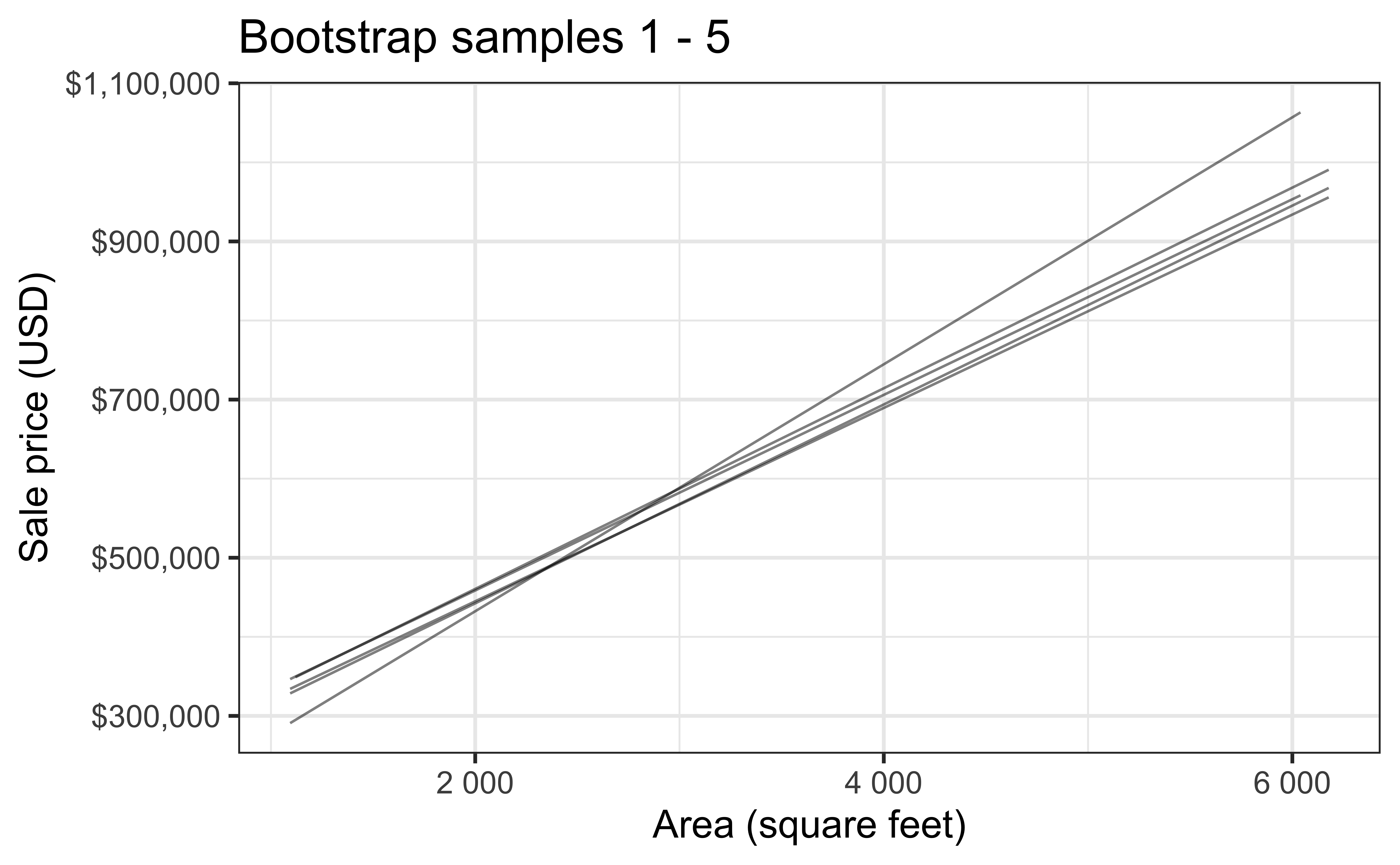

Bootstrap sample 1

Bootstrap sample 2

Bootstrap sample 3

Bootstrap sample 4

Bootstrap sample 5

so on and so forth…

Bootstrap samples 1 - 5

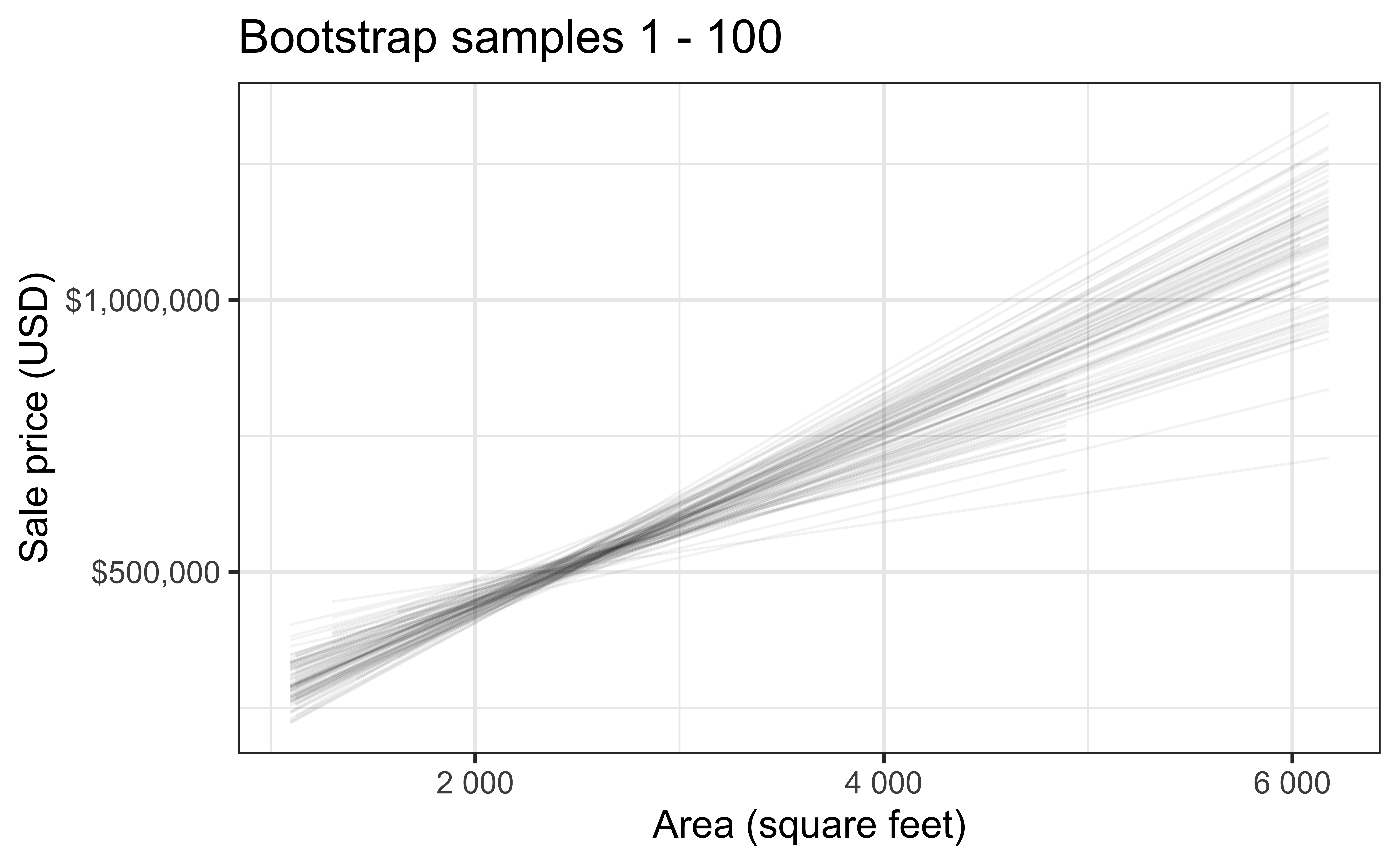

Bootstrap samples 1 - 100

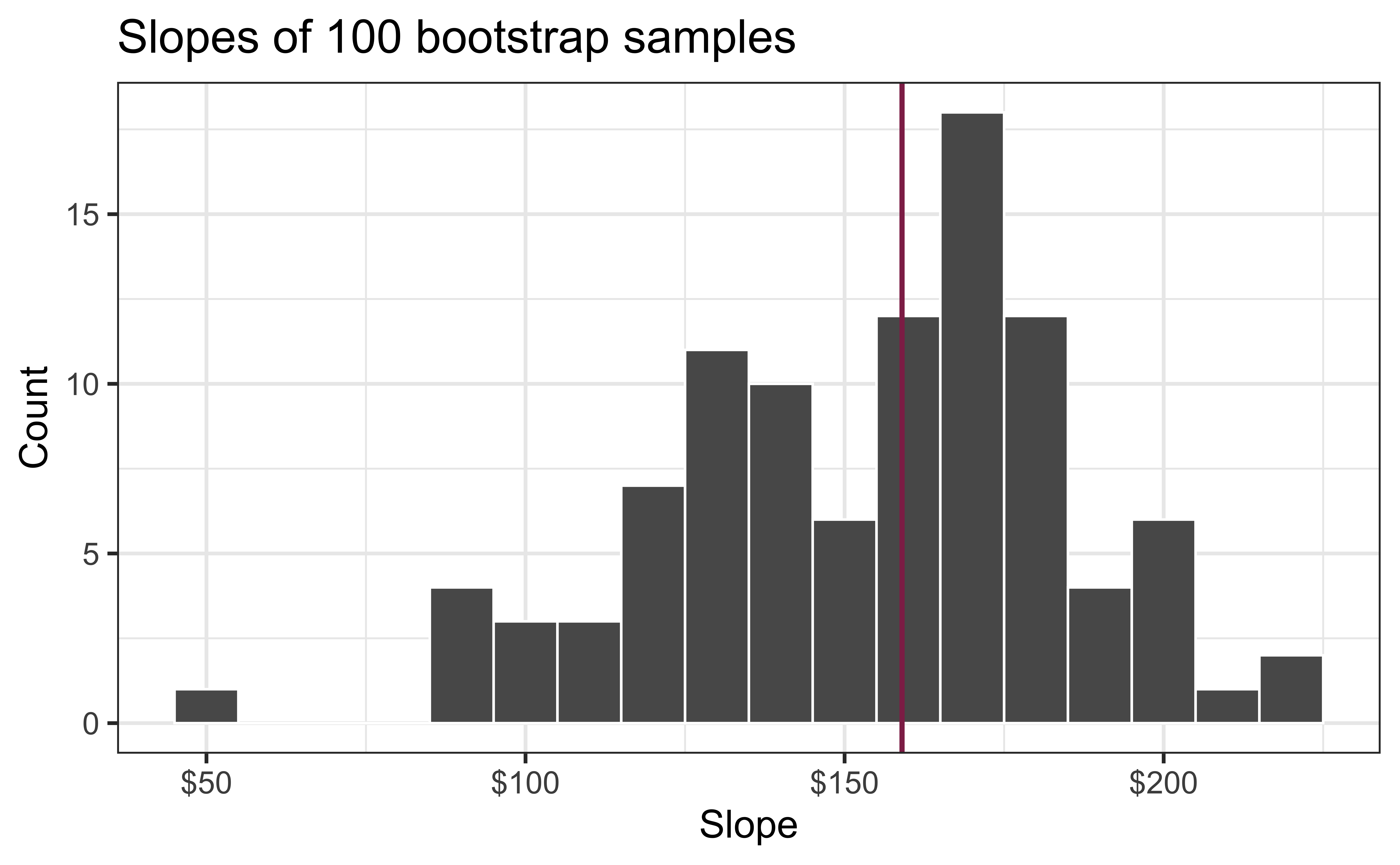

Slopes of bootstrap samples

Fill in the blank: For each additional square foot, the model predicts the sale price of Duke Forest houses to be higher, on average, by $159, plus or minus ___ dollars.

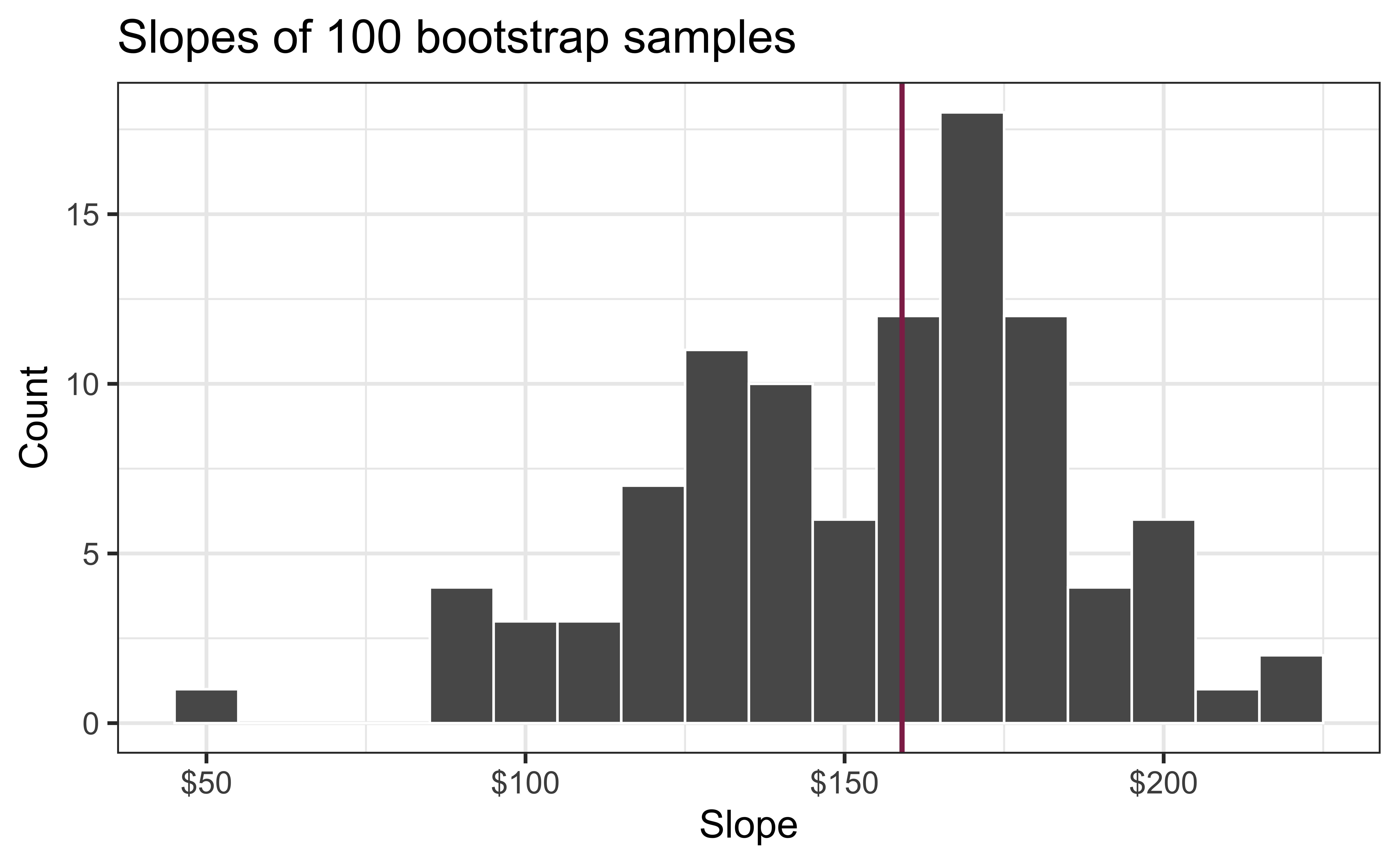

Slopes of bootstrap samples

Fill in the blank: For each additional square foot, the model predicts the sale price of Duke Forest houses to be higher, on average, by $159, plus or minus ___ dollars.

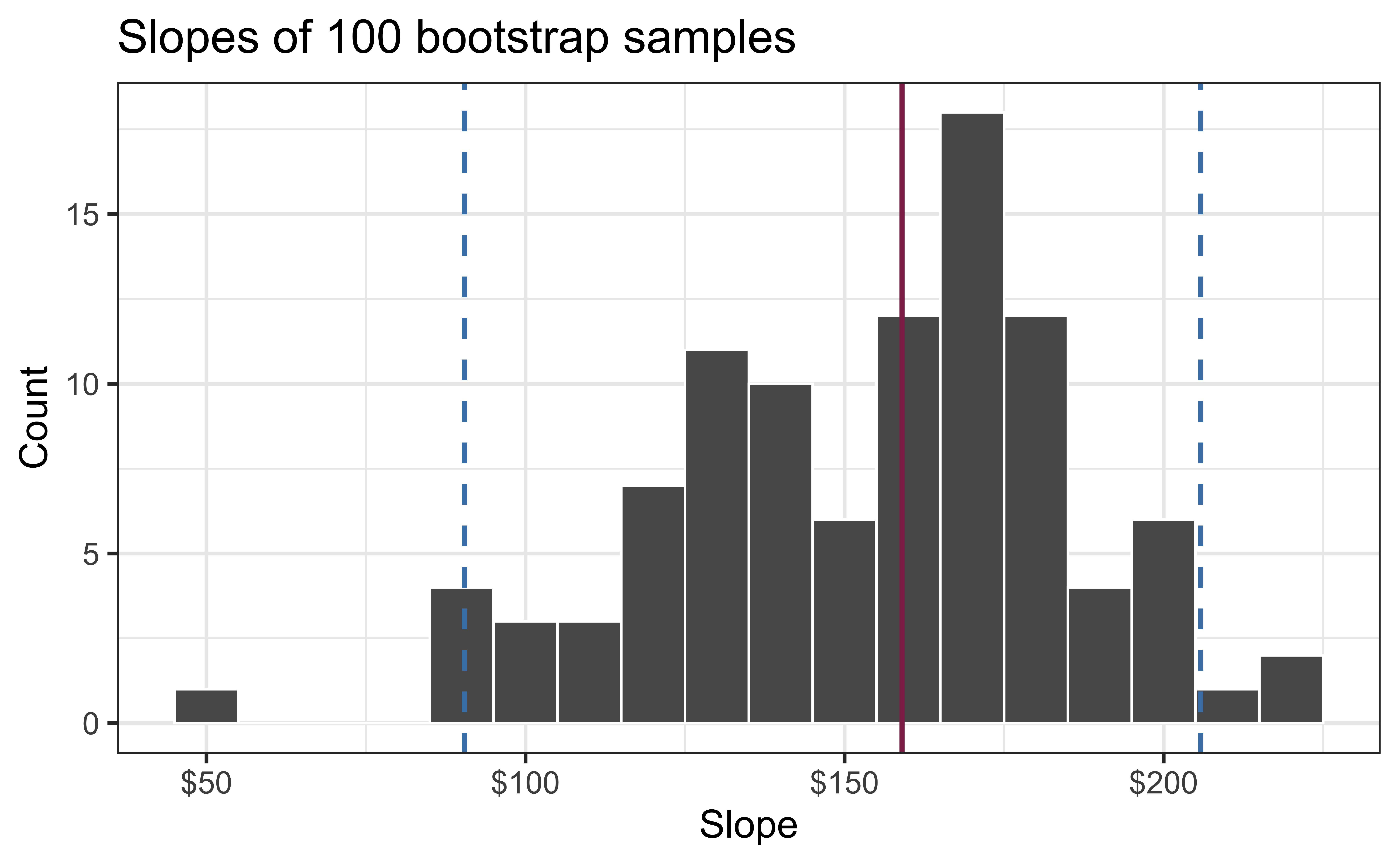

Confidence level

How confident are you that the true slope is between $0 and $250? How about $150 and $170? How about $90 and $210?

95% confidence interval

- A 95% confidence interval is bounded by the middle 95% of the bootstrap distribution

- We are 95% confident that for each additional square foot, the model predicts the sale price of Duke Forest houses to be higher, on average, by $90.43 to $205.77.

Precision vs. accuracy

If we want to be very certain that we capture the population parameter, should we use a wider or a narrower interval? What drawbacks are associated with using a wider interval?

Recap

Population: Complete set of observations of whatever we are studying, e.g., people, tweets, photographs, etc. (population size = \(N\))

Sample: Subset of the population, ideally random and representative (sample size = \(n\))

Sample statistic \(\ne\) population parameter, but if the sample is good, it can be a good estimate

Statistical inference: Discipline that concerns itself with the development of procedures, methods, and theorems that allow us to extract meaning and information from data that has been generated by stochastic (random) process

We report the estimate with a confidence interval, and the width of this interval depends on the variability of sample statistics from different samples from the population

Since we can’t continue sampling from the population, we bootstrap from the one sample we have to estimate sampling variability